India’s high growth, low inflation story at risk! RBI flags 5 adverse impacts from US-Iran war; how resilient is the economy?

")

The US-Iran war has caused major disruptions for global markets and economies, and India as the world’s fifth largest economy is not immune to the shock. Heavily dependent on imports to meet its crude needs, a rise in global oil prices above $100 per barrel and the supply bottlenecks created due to the de facto closure of Strait of Hormuz have hit various sectors of the economy. But how big is the hit likely to be? Is India’s growth story at the risk of being derailed by the Middle East conflict?The Reserve Bank of India in its first monetary policy review of 2026-27, while keeping repo rate unchanged, has expressed confidence in India’s fundamentals, firmly stating that they are on a ‘stronger footing’ at present than they have been in past crisis episodes as well as relative to many other economies. The central bank says that this strength provides it with greater resilience to withstand shocks,”

Keeping the ongoing West Asia crisis in mind, the RBI has estimated a 6.9% GDP growth for India in FY 2026-27 and an average inflation of 4.6%. These numbers assume an average oil price of $85 per barrel. The GDP growth for FY26 has been estimated at 7.6%. “Going forward, elevated energy and other commodity prices, as also shocks to availability of inputs due to disruptions in the Strait of Hormuz are likely to impact growth in 2026-27. The government has, however, been proactive in ensuring supply of inputs across critical sectors to minimise the impact of supply chain disruptions,” said RBI governor Sanjay Malhotra.“Sustained momentum in services sector, persisting impact of GST rationalisation, and healthy balance sheets of financial institutions and corporates should continue to support economic activity. The agricultural sector’s prospects are supported by healthy reservoir levels. Business expectations remain optimistic, and leading indicators point towards continued resilience in manufacturing and services sectors,” he said. “Moreover, the Government’s focus on scaling up domestic manufacturing in several strategic and frontier sectors augurs well for India’s ensuing growth trajectory,” he added.But even as it is confident of India’s ability to come out of the fresh global uncertainty, RBI has flagged five risks due to the US-Iran war that could negatively impact the economy.

RBI Flags 5 Risks

RBI’s message is clear: the initial supply shock can potentially transform into a demand shock over the medium term if the restoration of supply chains is delayed. RBI governor Sanjay Malhotra has listed five channels of transmission through which the Indian economy may take a hit due to the Middle East conflict. These are:Current Account Deficit:What the RBI governor said: Elevated crude oil prices could increase imported inflation and widen the current account deficit. What it means: The west Asia crisis has significantly impacted supplies of oil thereby raising the price of crude oil. Given that India is still a net energy importer , this will have a significant impact on the current account deficit, explains Vivek Iyer, Partner and Financial Services Risk Advisory Leader at Grant Thornton Bharat.

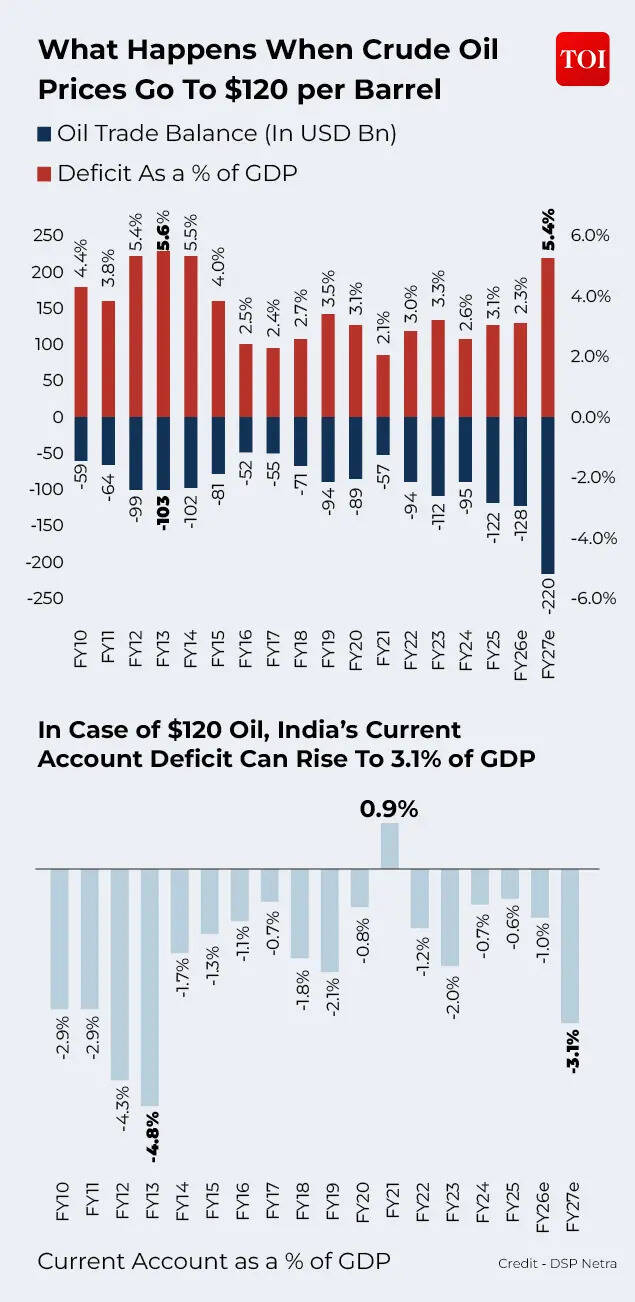

The numbers highlight the sensitivity:

- Every $10 increase in crude prices adds roughly $12–15 billion to India’s annual import bill.

- If crude prices were to rise towards $120 per barrel and sustain through FY27, India’s oil trade deficit could surge to nearly $220 billion, pushing the current account deficit above 3.1% of GDP, according to a DSP Netra report.

- Historically, such episodes have led to rupee depreciation of over 10%, alongside higher inflation and tighter liquidity conditions.

This makes crude oil arguably India’s largest macro variable outside domestic policy control.Impact of energy disruptionsWhat the RBI governor said: Disruptions in energy markets, fertilisers and other commodities may adversely impact industry, agriculture and services, reducing domestic output.What it means: Supply chain risks will cause the prices of commodities such as oil, fertiliser and other products that pass through the impacted shipping routes to increase resulting in imported inflation in India. Hence this is an upside risk to inflation, says Vivek Iyer.Safe Haven DemandWhat the RBI governor said: Heightened uncertainty, increased risk aversion and safe haven demand could impact domestic liquidity conditions, economic activity, consumption and investment. What it means: According to Iyer, this will result in foreign investment slowing down and money moving out of the country, elevating the currency risk exposure from a rupee depreciation standpoint.Reduced remittance flowWhat the RBI governor said: Weaker global growth prospects may dampen external demand and reduce remittance flows.What it means: ”This has the potential to impact inward remittances that today serve as a cushion against reduction in merchandise exports and rise in import costs of various commodities including oil and fertilisers amongst others,” the Grant Thornton Bharat expert says.

Higher cost of borrowingWhat the RBI governor said: Adverse spillovers from global financial markets could tighten domestic financial conditions and raise the cost of borrowing.What it means: ”Spill overs from international financial markets may raise the cost of borrowing in India – with risk aversion across, capital will be offered at a risk premium globally having a second order impact on rising cost of capital for India,” Iyer adds.

How big are the risks to India’s growth story?

DK Srivastava, Chief Policy Advisor, EY India notes that RBI’s projected effects on growth and inflation are asymmetric and depend primarily on the average global crude price which is assumed at $85 per barrel for 2026-27. “India’s real GDP growth is projected at 6.9% and CPI inflation at 4.6% for 2026-27. However, the RBI estimates that if the crude price averages $95 per barrel in 2026-27, growth would be lowered to 6.7% and inflation would be higher at 5.0%,” he says.“Given the required time lag for the global crude supply situation to normalize even if the crisis is resolved in the near future, there is a likelihood of average global crude price exceeding $95 per barrel in 2026-27. In such a scenario, India’s growth may be lowered further and inflation may be higher than the baseline projections,” he cautions.“Government policies to provide stability to prices may, however, moderate the impact on CPI inflation to some extent. The Monetary Policy Committee has not changed either the repo rate or the policy stance. It is only appropriate to wait for the next review meeting’s assessment of the situation regarding the crude price movements and its impact on inflation,” he adds.Ranen Banerjee, Partner and Leader, Economic Advisory Services at PwC India notes that crude oil prices above a certain level have had a broad based impact on the input prices for various industries that have petroleum based raw material usage. “Given the pressures on the external front, heightened inflation, stress on exporting entities and lower remittances besides constraints on government’s fiscal headroom to pump prime – will all have an impact on aggregate demand. This will constrain the ability of companies to pass on the higher cost of production to consumers and will therefore impact their margins,” he tells TOI.However, even though there are risks to the growth story, RBI and most economists are of the view that underlying domestic strength will help tide over the challenges.

According to Sachchidanand Shukla – Group Chief Economist at Larsen & Toubro, the RBI has rightly highlighted risks arising from the US-Iran war, but like the central bank, the economist is confident of India’s growth story.Firstly, it is important to note that the risks highlighted are real but largely priced in. India’s domestic-demand engine plus diversification limits growth downside to 6.5-6.9%, which is still one of the strongest large-economy prints globally, he tells TOI.He highlights possible mitigatory factors or offsets available as compared to the past. These are

- Oil & energy diversification possibility exists. Russia already has around 40% of crude basket (discounted barrels + SPR drawdown). UAE CEPA + accelerated GCC FTA talks cap dependence on West Asia at less than 35%.

- Fertiliser & critical inputs: Ramp-up from Russia/Canada plus PLI-linked domestic capacity (urea, NPK) already under way. Subsidy bill will rise but output loss will be capped at 10-15% vs 30% plus in past shocks.

- Trade & supply-chain resilience: Recent FTAs (Oman, UK, NZ) plus China+1/PLI momentum provide alternate sourcing lanes. The government is actively rerouting non-oil imports, he says.

- Policy space: Fiscal buffers (lower subsidy outgo in FY26) and RBI’s neutral stance give room for targeted liquidity support if liquidity tightens.

To sum it up, the imported inflation pass-through is likely limited to a 30-odd bps extra versus an unmitigated scenario. The Current Account Deficit stays manageable (<2% of GDP) with services exports and FDI continuing to cushion.However, breach of ceasefire or further escalation lasting beyond May and Brent crude prices of higher than $100 per barrel for a sustained period or rupee at over 95 will be the factors to watch out for, says Sachchidanand Shukla.Exuding confidence, Vivek Iyer, Partner and Financial Services Risk Advisory Leader at Grant Thornton Bharat sees the risks to India’s growth story as only a comma and not a full stop. “The fundamentals of the economy continue to be strong and supply side risks on account of geopolitical conflicts have already put India on a path to re-evaluate their trade relationships. This may potentially have an impact on the economic growth for a quarter as we pivot, but we see this impact only as a blip rather than a structural shift,” he tells TOI.In its monetary policy report released today, the RBI’s analysis clearly signals India’s resilience. “Domestic economic activity remains resilient, supported by robust private consumption and continued expansion in fixed investment, even as the external environment remains uncertain. Favourable agricultural prospects, steady services activity, elevated capacity utilisation and healthy balance sheets of corporates and banks are likely to underpin growth going forward. Continued public investment in infrastructure and recently concluded trade agreements are also expected to be conducive for medium-term growth prospects,” says RBI in its Monetary Policy Report at the start of the financial year.It warns that risks to the outlook persist. “Movements in crude oil prices and exchange rate developments warrant continued vigilance. Geopolitical tensions, volatility in global financial markets, uncertainty surrounding global trade policies and weather-related disruptions could pose headwinds to growth and inflation,” the central bank says. Over the medium-term, the growth-inflation dynamics would be conditional on when the supply chain is fully restored as well as where energy prices settle after the end of the West Asia conflict, it says.“At the current juncture, the situation is highly uncertain and would require continuous assessment of the developments to frame the appropriate policy response. Overall, India’s strong macroeconomic fundamentals and existing buffers provide resilience in the face of destabilising geopolitical developments and rising uncertainties,” it concludes.